The Trust Terms

Do the successor trustees, beneficiaries, distribution instructions, and disability provisions still match your wishes?

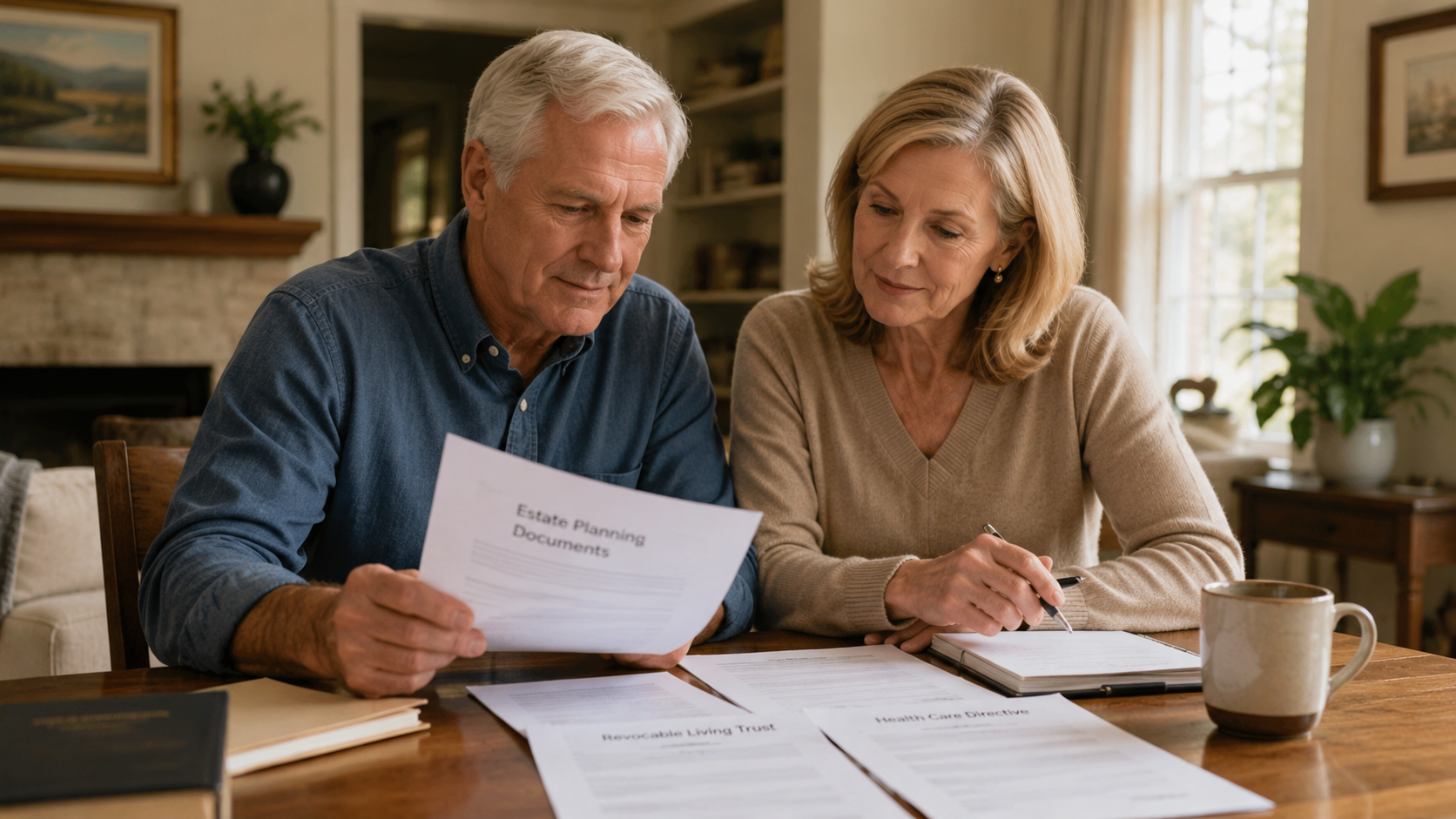

Living Trust Review

A living trust should not sit in a binder for 10 or 20 years without review. Your family, your assets, your health concerns, and the law can change. Your trust should keep up.

Plain-English Answer

You may not need to change your trust every few years, but you should review it regularly. A good review can help determine whether your trust still fits your family, your assets, your successor trustees, and your planning goals.

Why Updates Matter

Many people assume that once they sign a living trust, they are finished forever. That can be a dangerous mistake.

A trust prepared years ago may still be legally important, but it may not reflect your current family situation, your current assets, your current wishes, or your need for disability and long-term care planning.

The real question is not simply, “Do I have a trust?” The better question is, “Will this trust work when my family actually needs it?”

Common Reasons for an Update

A spouse has died, or you are now widowed.

You got married, divorced, or remarried.

A child, beneficiary, or successor trustee has died.

Your chosen trustee is no longer the right person.

You bought, sold, refinanced, or inherited real estate.

Your trust was never fully funded.

You want to change who receives your property.

You are concerned about nursing home costs or Medi-Cal planning.

Your powers of attorney or health care documents are outdated.

Your trust only focuses on death and does not address disability readiness.

Old Documents Can Create Confusion

If your trust has been sitting in a binder for years, it may no longer match your family, your assets, or your current planning needs.

Original Attorney Unavailable?

Many families have trusts prepared by an attorney who has retired, passed away, moved, stopped handling estate planning, or is simply no longer available.

That does not automatically mean the trust is invalid. But it can create problems when the family has questions, needs an amendment, discovers that assets were never funded into the trust, or realizes the documents no longer fit the family’s needs.

Miller Home Protection Law helps families review and update older living trusts, including trusts prepared by attorneys who are no longer available.

What Should Be Reviewed?

A proper trust review should not be limited to reading the first page of the trust. The whole plan should be reviewed together.

Do the successor trustees, beneficiaries, distribution instructions, and disability provisions still match your wishes?

Is the home properly titled? Are accounts and other assets coordinated with the trust?

Is the financial power of attorney strong enough for banks, real estate, care planning, and disability-related decisions?

Are your health care agents, HIPAA authorizations, and medical decision documents current?

Retirement accounts, life insurance, and annuities may pass by beneficiary designation, not simply by the trust.

Does the plan consider disability, nursing home costs, Medi-Cal planning, and protecting the family home before a crisis?

Warning Signs

What California families need to know the moment a loved one enters a nursing home. Enter your email and we’ll send it free.

✓ Check your inbox — the guide is on its way.

Your email is never shared. Unsubscribe any time.

What to Do Next

The worst time to discover an outdated trust is after disability, a nursing home crisis, a frozen account problem, or a death in the family.

A trust review can help identify problems before they become emergencies. Sometimes no major change is needed. Other times, an amendment, restatement, new power of attorney, updated health care directive, or trust funding work may be necessary.

Not sure whether your living trust is ready for disability, nursing home costs, or a family crisis? Get the free Home Protection Checklist and review the warning signs.

Get the Free Checklist

Client Education Guide — $29.95

An outdated living trust may still help avoid probate, but it may not fully address what happens when an aging parent needs help during life and an adult child steps in to manage money, accounts, care decisions, repairs, or the family home.

This guide explains the legal, financial, and family risks that can arise when helping children act without clear authority, strong documents, good records, and a plan that still fits the family’s current situation.

Miller Home Protection Law helps families review and update older living trusts so the plan is better prepared for life, disability, long-term care, and death.

(559) 625-4205